Hello Sovryn’s,

before our circle shows the first data analyses from the Subgraph, we would like to use this post to stimulate a discussion with regard to liquidity mining, the available supply and the fundamental value of the SOV token. We would like to use this post to prepare you for the discussions to come and to get you thinking.

We are very interested in your opinions. It makes little sense for our Circle to make suggestions that are met with majority disapproval in Bitocracy.

Of course, there are many nuances to this topic, but in this post we would like to present the problem as abstractly and simply as possible.

What gives the SOV token any value at all?

-

The Sovryn protocol charges fees. Since we are on a bitcoin layer, these are paid in btc. These fees are paid to SOV token stakers on a weekly basis. Staker revenue IN BTC determines the fundamental SOV value.

-

Further, control over the protocol code and proportional “ownership” of it also gives value to the SOV token (Governance power).

For now, all other incentives to give value or increase the value of the Sovryn token are speculative or a Ponzi.

This post is limited to point 1.

In simple terms, you can draw up an equation with the following declarations:

SOV token value ~ Staker revenue

Staker revenue = protocol revenue * staker share

SOV token value ~ protocol revenue * staker share

Explanation

People will buy SOV and stake it because they expect a weekly return in BTC. If this return is high enough, the demand for SOV will rise and with it, the token price.

Staker revenue: weekly bitcoin payout for a staker.

Protocol revenue: weekly protocol revenue from fees

Staker share: Staker SOV / total staked SOV

So let’s give this formula a thought:

SOV token value ~ protocol revenue * staker share

Assuming that protocol revenues are beyond our control, the only lever left is the staker share. If you increase this, the fundamental value of the SOV token increases. As the staker share depends on the total SOV that’s being staked, the SOV supply side comes into play. And with it, token inflation rate.

Next, I would like to give 2 abstract examples of how the token price is affected by a high (example 1) or moderate (example 2) token inflation rate and how the inflation rate plays into this scenario.

Example 1: Death spiral (invented numbers)

1:

Assuming a total of 10 million SOV are staked. Bob owns 100,000 staked SOV, i.e. 1% of the total number. We will leave the voting power formula aside. Bob receives 1% of the protocol revenue.

2:

Unfortunately, the SOV token is subject to a high rate of inflation, flooding the market with SOV. The Sovryn protocol borrows liquidity for their AMM pools by paying SOV rewards. After one month, there are no longer 10 million, but 20 million staked SOV tokens. Bob receives only 0.5% of the profit, his APY went down 50% because there is more staked SOV.

3:

He could buy more SOV to add to his weekly profit but he knows that in another month 30 million SOV will be staked. His weekly return will continue to decrease if the platform revenue does not skyrocket as much as the token supply. He decides to give up his position and sells the SOV.

4:

The selling pressure causes the token price to drop. Since SOV is also used to borrow liquidity for the platform, as the SOV price falls, the yield in the pools decreases and liquidity is withdrawn. As a result, the platform volume falls and stakers receive fewer weekly rbtc payouts. More stakers give up their positions and sell their SOV. The price falls, the AMM pool liquidity falls because the liquidity mining rewards become less attractive, the platform volume falls due to lower liquidity. The protocol is caught in a death spiral. Caused by a high token inflation rate. The fiat system sends its regards.

High token inflation => More SOV getting staked => reduced staker revenue => reduced token price => reduced AMM APY => reduced liquidity/volume => Higher SOV borrowing cost for AMM liquidity => higher token inflation

Example 2: The flywheel

1:

A total of 10 million SOVs are staked. Bob owns 100,000 staked SOVs, i.e. 1% of the total number. We will leave the voting power formula aside. Bob receives 1% of the protocol revenue.

2:

Due to liquidity mining rewards, there is a moderate token inflation rate. It is expected that by the next month, there will be 11 million token staked instead of 10. Bob really likes his weekly btc payouts and he wants to keep his 1% of total fee share. He decides to buy 10000 SOV from his btc staker payouts and other capital in this month so that he keeps his 1% fee share. The token price increases slightly because the good rewards provide demand for the token.

3:

With a relatively stable or increasing SOV token price that’s backed by good staking rewards, liquidity mining on the protocol is really profitable. A lot of people want to farm valuable SOV tokens. The liquidity pools increase in size and with good marketing, the platform volume grows. SOV stakers receive even higher rewards which increases demand for the token. The high token price lets the AMM pool APY’s rise. The SOV rewards for the pools get adjusted so the APY stays at good but not insanely high levels.

4:

A reduction of SOV rewards for liquidity mining is possible while growing/keeping the liquidity. It reduces the token inflation rate and the potential amount of staked SOV while maintaining competitive AMM pool APY’s. This makes SOV a valuable and scarce asset due to it’s underlying promise of high weekly btc payouts.

Higher staking rewards => Increasing token price => increasing AMM pool APY => reduced amount of SOV used to borrow AMM pool liquidity => Reduced token emission => Less staked tokens => higher staking rewards.

Or

Higher staking rewards => Increasing token price => increasing AMM pool APY => AMM pools grow => higher volume => higher staking rewards

The flywheel takes off.

Thoughts

The liquidity mining reward program pays out 450.000 SOV per month in order to attract/borrow liquidity. (Some of this SOV gets sold on the market, some of it gets staked. The circle is working to provide the accurate data.)

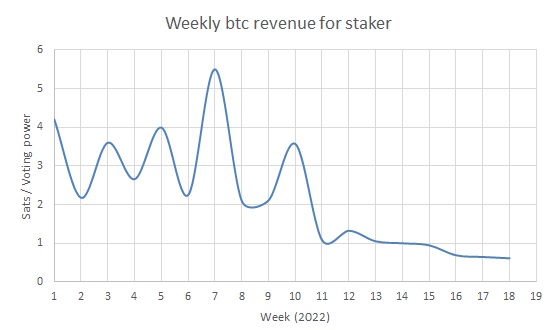

With relatively constant Dapp volume, staker revenue in btc dropped significantly throughout 2022 because there is more SOV staked. Note week 7 and note the week 16 top.

Let’s compare this with our Example 1:

More and more SOV gets staked, but the average return for a staker is down a lot in recent weeks. Example 1 Point 2 has taken place. According to the voluntarily staked SOV chart, we cannot say if Example 1 Point 3 is already taking place but we could be close to it. The AMM and lending pool liquidity remains relatively constant for now (Circle is working on providing this data) even though the APY in the pools is in a downtrend (Circle is also working on this data). The death spiral is not here yet because the pools are still looking good. But there is a significant risk!

We have a high token inflation rate from liquidity mining already and yet, the pool APY continues to slowly bleed down. In addition, we have a significant reduction of staker btc revenue which is only going to get worse with more SOV hitting the open market.

The million dollar question: How do we get out of Example 1 and enter Example 2?

To enter Example 2, these things have to happen:

-Staker revenue stops going down and starts increasing.

-Token inflation rate needs to go down or at least does not lead to reduced staker revenue.

-SOV token price must increase.

What are the hurdles?

-Simply cutting off LM rewards and reducing token inflation has a high risk of losing liquidity and with it, platform volume/staker revenue.

-Reducing inflation rate may not directly increase token price or staker revenue while having a direct impact on liquidity.

-Staking revenue will take a lot to get to attractive levels again with all the SOV that’s already staked. The amount of staked SOV is not very high compared to overall already liquid SOV supply that can potentially be staked.

What are the options to reach Example 2?

-Increased platform revenue: This may happen with Zero/Perps/limit orders. IF this happens, we may have a chance to start the flywheel. We have to be prepared to react with regard to LM rewards if we see an uptick in platform revenue. We must have the data analysis ready and we must have plans that can be executed and monitored/adapted.

-Create a supply shock by locking up a significant amount of SOV for a long time. According to Example 2 Point 2, Bob would be inclined to add to his stake instead of selling off if he knows that there is not going to be much more SOV available for staking in the next years.

-Create a hype and surge in token price. Reduce LM rewards and token inflation so that AMM pools remain on a reasonable APY while reducing token inflation rate. Example 2 Point 3+4. A hype can also be created by the announcement of locked up or even burned tokens. An impulse to make the wheel turn in the right direction.

-Reducing LM rewards but give LM providers attractive options to keep their liquidity on the AMM pools. Liquid rewards, no vesting schedule could be an option.

-Reducing LM rewards by reducing unprofitable pools on purpose. ETH/BTC or BNB/BTC are very unprofitable and pay high SOV rewards. We could cut rewards in half and be happy with half the liquidity in these pools. Tighten and focus the liquidity on profitable pools. IF we reduce LM rewards by 50% and as a reaction, 50% of liquidity gets withdrawn, the remaining liquidity still enjoys the same APY as before such measure. According to recent trading volumes in these pools, there’d not be much risk of losing volume due to lower liquidity because the volume is much lower than available liquidity. (I know, the Circle also has to provide this data and we’re working on it but it’s a lot of work to do.)

Please add thoughts and critics!

Stay Sovryn!